Credit Scores Demystified: Habits That Move the Needle

Demystify your credit score with simple, proven habits, from on-time payments to smart utilization, that can raise your number fast and keep it strong.

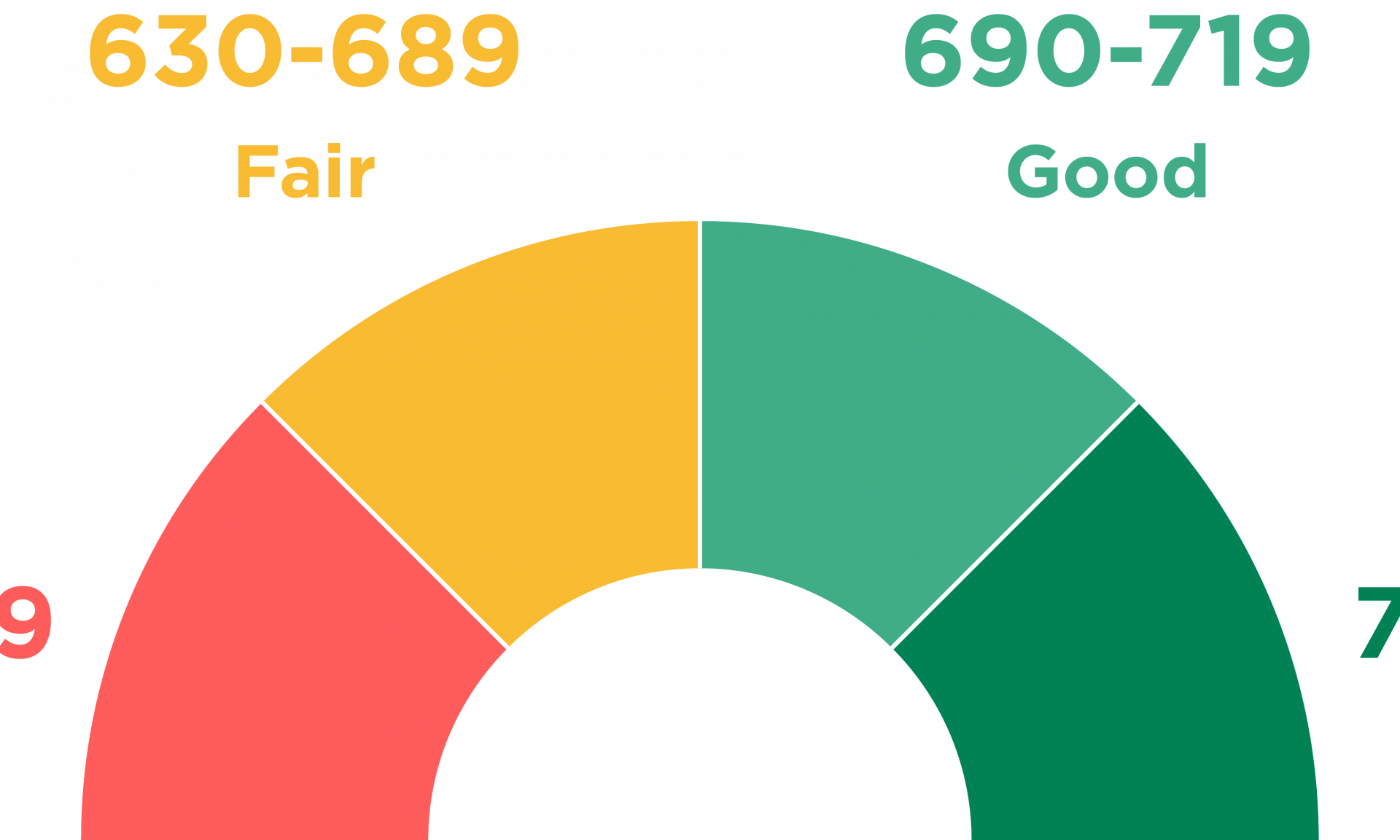

What Your Credit Score Really Measures

Your credit score is a quick snapshot of how you manage borrowing in personal finance, distilling long-term habits into a single number lenders use to gauge risk. Under the hood, several levers work together. The heavyweight is payment history, a record of whether you pay on time. Close behind is credit utilization, the share of revolving limits you use. Then comes length of credit history, which rewards seasoned accounts, and credit mix, reflecting how you handle both revolving and installment obligations. Finally, new credit activity, including hard inquiries, signals how frequently you seek fresh lines. None of these levers exists in isolation; they interact daily with every swipe, statement, and transfer. Demystifying them turns a mysterious score into a set of navigable dials. When you know which behaviors shift which dial, you can build routines that steadily reduce risk, improve terms, and free up cash flow for goals like savings, investing, and resilience against surprises. Scores respond to stability more than drama; consistent small wins outrun flashy one-off moves.

Never Miss a Payment: Systems That Stick

Because payment history drives so much of your score, build a fail-safe system that prevents slips. Start with autopay for at least the minimum on every account, then schedule a second manual sweep to pay the remainder. Align due dates with your paycheck rhythm so cash flow supports punctuality, and keep a small buffer in checking to absorb timing hiccups. Set layered reminders across calendar apps and banking alerts, and consider consolidating due dates to reduce mental overhead. If life throws a curveball, contact your issuer before a bill is late; asking for a temporary hardship plan or interest concession can preserve your record. Avoid returned payments by confirming available funds before initiating transfers. For installment loans, enable e-bills so statements surface where you manage money already. Treat new charges as already spent, not future-you's problem, and let on-time payments become a quiet routine. The habit is simple, but its compounding effect on your credit standing is powerful.

Mastering Utilization: Balances, Limits, and Timing

Your credit utilization ratio is the portion of revolving credit you are using, and lower is better for your score. Two actions move this needle fast. First, control balances: plan purchases, split big expenses across cycles, and use mid-cycle payments to keep reported amounts calm. Second, mind timing: the statement closing date is when many cards report balances, so paying before that date can present a leaner snapshot. If your spending is steady, consider multiple small payments each month to flatten peaks. You can also ask for a higher limit to reduce the ratio, but weigh the potential for a hard inquiry and only request what aligns with your budget. Spreading recurring bills across more than one card can reduce spikes, though simplicity matters too. Remember that utilization is about reported balances, not whether you pay in full. Use cards as a tool, not a tab; transact, then clear. Over time, calm utilization signals low risk and elevates your profile.

Age and Mix: Building Depth Without Drama

Lenders like to see that you can manage different types of credit over time, so cultivate length of credit history and a healthy credit mix without unnecessary complexity. Keep older, no-fee cards open and active with a small recurring charge to preserve account age and continuity. If you are building from scratch, a secured card or a credit-builder loan can seed positive data; use them sparingly, pay predictably, and let time do the heavy lifting. Becoming an authorized user on a well-managed, low-utilization account can add depth, provided the primary user has strong habits. Add installment credit only when it serves a real goal, like transportation or education, and avoid opening several accounts in a short window just to diversify. Closing an account may shorten average age and reduce total limits, so run a cost-benefit check first. Patience matters here: aging a file takes seasons, not days, and steady stewardship quietly strengthens the foundation of your credit story.

Apply Smart, Monitor Smarter

New applications create hard inquiries and new tradelines, so space them thoughtfully and apply with purpose. Use prequalification tools that rely on soft checks when exploring options, and batch needs around clear goals rather than impulse upgrades. After any approval, resist the urge to celebrate with spending; let the new limit improve utilization while your behavior stays boring. On the monitoring side, review your credit reports regularly, verify personal details, and dispute errors promptly with clear documentation. Set up account alerts for large transactions, international activity, and changes to personal data. If you spot suspicious behavior, consider a fraud alert or a credit freeze to block unauthorized accounts while you investigate. Keep a simple tracker of open accounts, due dates, and limits so you can see how actions ripple across your profile. Above all, be patient. Scores reward steady, low-drama habits that support your broader financial plan, from emergency funds to long-term investing.